What does the Stamp Duty Tax Break mean for landlords looking to expand their portfolios?

In a bid to stimulate the struggling property market, the Chancellor Rishi Sunak announced on 8th July 2020 a new stamp duty tax break. Property investors who purchase through limited companies will only incur the 3% surcharge on purchases (above the £40,000 exemption) and will no longer be required to pay the additional rates for all purchases completed before 31/03/2021.

In this article, we look at what that means for landlords looking to expand portfolios and purchase additional properties through limited companies.

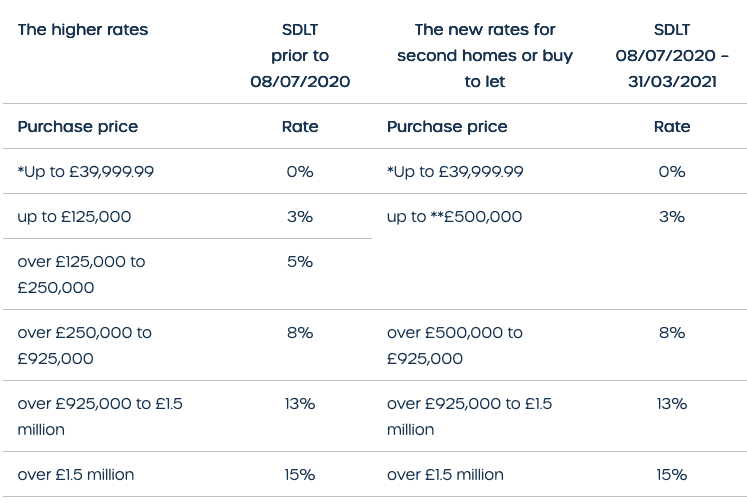

Below we have a comparison tax table showing the rates you would have paid when completing on a second property or buy-to-let up to 8th July 2020 vs the new rates applicable between 08/07/2020 – 31/03/2021:

*Properties purchased under £40,000 do not incur SDLT. If the purchase price is £40,000 or over, SDLT is payable on the full purchase price.

**Don’t forget the Annual Tax on Enveloped Dwellings kicks in over £500k.

From 8th July 2020 until 31st March 2021 if you complete on a second home or buy-to-let purchase in the UK with a purchase price between £40,000 and £500,000, you will only be required to pay 3% stamp duty land tax on the purchase price and not the previous higher rates.

What does that look like in reality?

A home worth £300,000, that is not a main residence which includes second homes and investment purchases, the stamp duty bill would be £9,000 instead of £14,000. This is because the three per cent surcharge on second homes is still applicable. But normal stamp duty rates do not apply.

For a purchase of a £500,000 property, the £30,000 tax bill would be cut in half.

Why should I buy an investment property through a limited company?

As a property investor with multiple sources of income, setting up a company could limit your personal tax bill (although please be aware it depends on your personal circumstances and the type of property business you will have).

If you own buy-to-let properties personally the rental profits are taxed at your personal tax rate. Capital gains will be taxed at 18% – 28% depending on your taxable income. The capital gain in a limited company will be charged at the corporation tax rate of 19%.

It is important to understand the advantages, disadvantages and responsibilities associated with Limited company ownership of buy to rent properties.

I already own the buy-to-let property, should I transfer it into a limited company?

The stamp duty window will give landlords the opportunity to move properties from their own name into limited companies which they may not have done previously due to the stamp duty implications.

From April 2020 if you owned the buy-to-let property in your personal capacity you would no longer be able to offset the mortgage interest payments as a qualifying expense against rental income in your self-assessment tax return. This is not the case for companies that hold property, meaning the mortgage interest payments will remain an allowable business expense to reduce profits and in turn reduce corporation tax.

Still to consider when you think about transferring properties into a limited company:

- The company would be liable to pay Stamp Duty of 3% where the property value is greater than £40,000;

- You may have to pay up to 28% capital gains tax (CGT) on the difference between your original purchase price and your sale price;

- You will need to pay conveyancing and potentially mortgage transfer costs;

These two tax drawbacks could potentially wipe out any savings from claiming interest tax relief on your finance costs. We would recommend you do an analysis of the tax consequences before you do the transfer.

I am considering a property purchase through a limited company, what are my next steps?

Contact our SAIL team who will be able to assist you with the setup of a UK limited company along with the associated business bank account and ensure your company meets its necessary annual statutory requirements. We’ll also put you in touch with our team of trusted advisors to arrange the right mortgage & protection cover for you.

I am considering transferring my existing buy-to-let property into a limited company, where do I go from here?

Give us a call, we’d be happy to provide a calculation for you on your estimated taxes to make this change as well as assist you with getting setup with a limited company if this is the most beneficial route for you.